Roofing Insurance Claims Assistance in Johns Creek, GA

We manage every step of your roofing insurance claim — from damage documentation and adjuster meetings to HOA coordination in Country Club of the South, St. Ives, Abbotts Bridge, and Medlock Bridge.

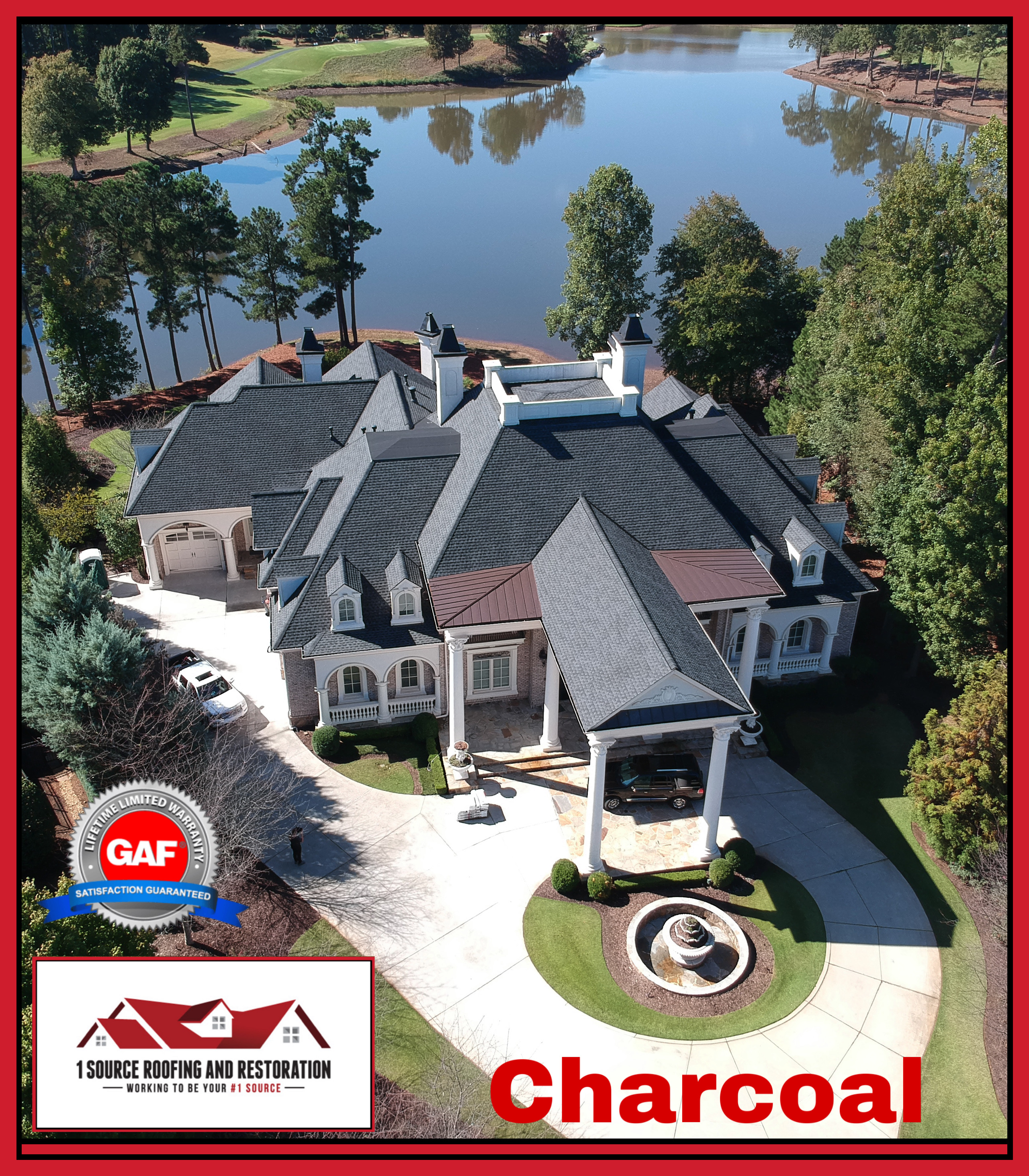

Certified by Industry-Leading Manufacturers

Why Roofing Insurance Claims in Johns Creek Require a Specialist

Johns Creek is one of the most affluent cities in Georgia, and its roofing insurance claims reflect that complexity. Homes in gated communities like Country Club of the South and St. Ives routinely carry replacement values above $1 million, and a single roof restoration can involve $30,000 to $80,000 or more in insured work. When stakes are this high, the difference between a correctly filed claim and an underpaid one is significant — and insurance adjusters know it.

Many Johns Creek homeowners discover only after the fact that their adjuster missed line items, applied excessive depreciation, or failed to account for the premium materials required by their HOA's architectural standards. A GAF Timberline HDZ roof that costs $18 per square foot is not interchangeable with a standard three-tab shingle — yet generic estimates are common. Our team reviews every line of your Explanation of Benefits and identifies discrepancies before you sign anything.

Beyond the insurer, Johns Creek homeowners face a second regulatory layer that most roofing contractors are not equipped to manage: homeowners association approval. In Country Club of the South, St. Ives, Abbotts Bridge, and Medlock Bridge, every exterior material change requires architectural committee sign-off. We prepare your HOA submission in parallel with your insurance claim so you are not waiting weeks for committee approval after the insurer has already paid.

Managing the Dual Process: HOA Approval and Insurance Claims Simultaneously

Most roofing contractors handle one process at a time — they wait for the insurance claim to settle before approaching the HOA. This sequential approach adds four to eight weeks to your project timeline and leaves you exposed to weather damage on a compromised roof. We run both tracks in parallel from day one.

The Insurance Track

We begin with a thorough roof inspection using calibrated hail gauges, moisture meters, and drone imaging. Every impact point, granule loss pattern, and structural deformity is photographed and documented in a written report that matches the format adjusters use in their own damage estimates. When your adjuster arrives on-site, we are there with our report. We walk the roof together. We point out damage that a quick visual inspection would miss. We do not leave until every item of damage is acknowledged.

If the initial estimate falls short — and it often does with hail damage on premium roofing systems — we prepare a supplemental claim supported by our documentation and submit it directly to the insurer's desk adjuster. We handle all back-and-forth communications so you are not fielding calls from adjusters and third-party claim reviewers on your own.

The HOA Track

Simultaneously, we identify replacement materials that are pre-approved or easily approvable by your community's architectural committee. For Country Club of the South and St. Ives homeowners, this typically means Boral or GAF architectural shingles in a palette that matches the existing streetscape. We prepare the full architectural review application: material samples, color swatches, manufacturer specification sheets, and installation method documentation. We submit on your behalf and track approval status.

In most cases, HOA approval arrives before the insurer has processed the full claim — meaning the moment your check clears, we are ready to schedule installation without any additional waiting period.

Johns Creek Neighborhoods We Serve

Our familiarity with Johns Creek's residential communities goes beyond knowing the zip code. We understand the specific HOA structures, roof age profiles, and common storm damage patterns in each area.

Country Club of the South

One of the most prestigious gated communities in north Fulton County, Country Club of the South was largely built between 1988 and 1999. A significant share of its homes now carry roofs that are 25 to 35 years old — well past the manufacturer's expected lifespan for standard asphalt shingles. The community's HOA maintains strict standards for roofing materials, colors, and installation methods. We have prepared successful architectural review applications for this community and know what the committee requires for fast approval.

St. Ives Country Club

St. Ives homes built in the early-to-mid 1990s face the same roof age dynamic as Country Club of the South. Many homeowners here are filing their first-ever roofing insurance claim and are unaware that their 30-year-old roof, despite its age, may qualify for full Replacement Cost Value coverage if the damage was caused by a covered peril — typically hail or high winds. We review your policy language with you before filing so there are no surprises.

Abbotts Bridge and Medlock Bridge

These communities span the Johns Creek and Duluth corridor and include a mix of homes built from the mid-1990s through the mid-2000s. Both areas experienced significant hail activity during the 2022 and 2023 storm seasons. If your roof sustained impact damage during those events and a claim was not filed within the policy's discovery window, your options may now be limited — but we can review your current policy, identify any active damage, and advise on the most effective path forward.

What We Handle on Your Behalf

From the first phone call to the final nail, we manage the full claims and restoration process.

Damage Documentation

Comprehensive roof inspection with calibrated hail gauges, drone imaging, and a written damage report formatted for insurer review. We photograph every impact point so nothing is omitted from your claim.

Adjuster Meeting Representation

We attend your adjuster inspection as your roofing advocate. We walk the roof alongside the adjuster, present our findings, and ensure every item of legitimate damage appears in the scope of work.

Supplemental Claims

When the initial estimate misses items or underpays, we submit documented supplemental claims directly to the insurer's desk adjuster. We handle all follow-up correspondence until the scope is complete.

HOA Architectural Review

We prepare and submit your HOA approval application in parallel with the insurance claim — including material samples, specifications, and color documentation for communities like Country Club of the South and St. Ives.

Policy Review and Guidance

Before filing, we review your policy to identify whether you have RCV or ACV coverage, understand your deductible structure, and advise on whether a claim is the right financial decision for your situation.

Premium Material Installation

Once the claim is approved, our GAF-certified installation crews restore your roof with materials that meet both your insurer's requirements and your HOA's architectural standards — no shortcuts, no substitutions.

Understanding Hail Damage on Johns Creek's Aging Roof Stock

Johns Creek and the broader north Fulton County corridor sit in a hail corridor that experiences moderate-to-severe hailstorms multiple times per decade. The 2022 and 2023 spring storm seasons were particularly active, with documented hail exceeding 1.5 inches in diameter in areas including Alpharetta, Johns Creek, and the SR-120 corridor.

On a newer roof, hail damage is visible: cracked, dented, or missing shingles, granule loss that exposes the mat beneath, and bruising that can be felt by pressing a fingertip into the shingle surface. On an older roof — particularly the 25 to 35-year-old roofs common in Country Club of the South, St. Ives, and Abbotts Bridge — the picture is more complex. Age-related granule loss can mask hail impact patterns. Borderline-condition shingles deteriorate rapidly after a hail event, even if the visual impact was not dramatic at the time of the storm.

This is why professional documentation matters. Our inspection process uses calibrated hail gauges to measure impact crater dimensions and pattern density — the same methodology used by independent insurance engineering firms. When our report is in hand, there is no ambiguity about whether the damage is hail-caused versus age-related deterioration. Insurers must respond to documented evidence.

What Counts as a Covered Peril

Standard Georgia homeowner's policies cover direct physical damage caused by a sudden, accidental event — including hail, wind, fallen trees, and ice damming. They do not cover normal wear and tear, gradual deterioration, or maintenance neglect. The line between "hail-accelerated deterioration" and "normal aging" is often contested by insurers, and it is the single most common reason legitimate claims are denied or underpaid. Our documentation is specifically designed to establish the causal link between a specific storm event and specific damage — not general roof condition.

The Depreciation Question

If your policy provides Replacement Cost Value (RCV) coverage, your insurer pays the full cost to restore your roof to its pre-loss condition with materials of like kind and quality — regardless of your roof's age. They initially pay the Actual Cash Value (ACV), which is the RCV minus depreciation, and release the withheld depreciation (called recoverable depreciation) after the work is completed. If your policy provides only ACV coverage, the withheld depreciation is not recoverable. Understanding which type of policy you hold changes the financial calculus of filing a claim, and we review this with every Johns Creek homeowner before submitting anything.

Our Insurance Claims Process for Johns Creek Homeowners

We have refined this process across hundreds of claims in metro Atlanta. Every step is designed to minimize your time commitment and maximize the accuracy of your claim outcome.

- Free Roof Inspection: We conduct a full inspection of your roof and exterior, document all damage with photographs and written notation, and provide you with a clear picture of what was found — at no charge and with no obligation to proceed.

- Policy Review: We review your homeowner's policy with you, confirm your coverage type (RCV vs. ACV), identify your deductible, and advise whether filing a claim is in your financial interest given your specific situation.

- Claim Filing Support: We help you file your claim with your insurer, provide your damage report as supporting documentation, and ensure the claim is positioned correctly from the first submission.

- Adjuster Meeting: We attend your insurance adjuster inspection as your roofing representative, walk the roof alongside the adjuster, and present our damage documentation to ensure all items are captured in the scope of work.

- Scope Review and Supplemental Claims: We review the insurer's written estimate against our scope and file supplemental claims for any missing or underpaid line items. We manage all correspondence until the scope is finalized.

- HOA Approval Submission: In parallel, we prepare and submit your HOA architectural review application with all required documentation, track the review, and respond to any committee questions.

- Premium Installation: Once approvals are in place, our certified installation crews complete your roof restoration using approved materials, with all work backed by manufacturer warranties and our workmanship guarantee.

- Final Documentation: We provide you with a complete project file — photographs, material specifications, permit records, and warranty documentation — so you have everything you need for your insurance records and future resale.

Start Your Free Roof Inspection Today

Serving Country Club of the South, St. Ives, Abbotts Bridge, Medlock Bridge, and all of Johns Creek. Our team is ready to assess your roof, review your policy, and guide you through every step of the claims process.

Call (404) 277-1377What Sets Our Claims Advocacy Apart in Johns Creek

There is no shortage of roofing contractors in north Fulton County. What separates us is not marketing language — it is the specificity of what we do and the depth of our knowledge of local conditions, community requirements, and insurance claim mechanics.

- We know Johns Creek's HOAs: We have submitted architectural review applications to multiple Johns Creek HOAs and understand what each committee requires for fast approval. We do not learn your community's standards on your project.

- We attend adjuster meetings: Many contractors submit documentation and hope for the best. We are physically present at your adjuster inspection as your advocate — because in-person representation changes outcomes.

- We know Georgia insurance policy language: RCV vs. ACV, recoverable depreciation, ordinance or law coverage, code upgrade requirements — these terms have real dollar implications. We explain them clearly and use them correctly in claim submissions.

- GAF-certified installation: Our installation teams are GAF Certified, which means your completed roof qualifies for GAF's full system warranty — the kind of documentation that matters when you sell a home in Country Club of the South or St. Ives.

- We do not work for the insurer: We are your contractor. Our job is to make sure your claim accurately reflects the full scope of your damage and that your roof is restored to the standard your home requires.

- No upfront cost for inspections or claim support: We conduct your roof inspection and provide claims assistance at no charge. We are paid through the roofing contract when the work is approved and completed.

Learn More About Our Services in Johns Creek

Explore related pages to understand the full scope of what we offer for Johns Creek homeowners.

Frequently Asked Questions

Answers to the questions we hear most from Johns Creek homeowners navigating the insurance claims process.

Will my Johns Creek HOA complicate my roofing insurance claim?

HOA requirements do not prevent you from filing a valid insurance claim — they run on a parallel track. Your insurance covers the cost of restoring your roof to its pre-loss condition. Your HOA governs which materials and colors are permitted. We work with both simultaneously: we submit your claim documentation to the insurer and prepare the HOA approval application at the same time, so both processes move forward without adding weeks to your timeline. In most cases, we can identify HOA-approved materials that your insurer will fully cover.

My Johns Creek roof is from the mid-1990s. Can I still file a hail damage claim?

Yes, though the outcome depends on your policy type. Homes in Country Club of the South, St. Ives, and Abbotts Bridge that were built between 1991 and 1998 often have roofs that are now 25 to 30 years old. If your policy provides Replacement Cost Value (RCV) coverage, your insurer must pay to restore the roof to current standards regardless of age. If you have Actual Cash Value (ACV) coverage, the payout will be reduced by depreciation. We review your policy with you before filing and advise on whether a claim is financially beneficial — there is no obligation.

What does 1 Source Roofing do at an insurance adjuster meeting in Johns Creek?

We attend the adjuster inspection as your roofing advocate. Before the meeting, we complete our own detailed damage assessment and photograph every point of impact, granule loss, and structural compromise. During the adjuster meeting, we walk the roof alongside the adjuster, point out damage that is easy to miss from a quick inspection, and provide our written report. If the adjuster's scope undervalues the damage, we submit a formal supplemental claim supported by our documentation. Our goal is to make sure nothing is left off the estimate.

How long does a roofing insurance claim take in Johns Creek, GA?

A straightforward claim — where damage is clear and the insurer agrees with the scope — typically takes three to six weeks from initial filing to receiving your Explanation of Benefits. Add one to two weeks for HOA architectural review if your community requires it. If supplemental claims are needed, investment another two to four weeks. We keep you informed at every step and handle all insurer and HOA correspondence on your behalf, so you are not managing timelines or paperwork on your own.

Insurance Claims Resources

Explore our complete library of insurance claims guides, tools, and resources to help you navigate your roofing claim with confidence.